🟢 Speak with an agent today!

Navigating the Landscape of Medicare Insurance Premiums

Navigating the Landscape of Medicare Insurance Premiums

Medicare insurance premiums are a crucial aspect of healthcare planning for many individuals, particularly those aged 65 and older. Understanding the various components, costs, and factors influencing these premiums is essential for making informed decisions and ensuring adequate coverage. In this article, we delve into the nuances of Medicare insurance premiums, providing insights and information to help you navigate this complex landscape.

Understanding Medicare Insurance Premiums

Medicare is a federal health insurance program in the United States, primarily serving individuals aged 65 and older, as well as certain younger individuals with disabilities. The program is divided into different parts, each covering specific healthcare services, and the premiums associated with these parts can vary.

Part A: Hospital Insurance

Medicare Part A covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care. Most individuals do not pay a premium for Part A if they or their spouse have paid Medicare taxes for a certain period while working. However, for those who do not qualify for premium-free Part A, the cost can be up to several hundred dollars per month.

Part B: Medical Insurance

Medicare Part B covers outpatient care, doctor's services, preventive services, and some home health care. The standard Part B premium amount is determined annually by the government and can change each year. Individuals with higher incomes may pay an Income-Related Monthly Adjustment Amount (IRMAA), resulting in a higher premium.

Part C: Medicare Advantage

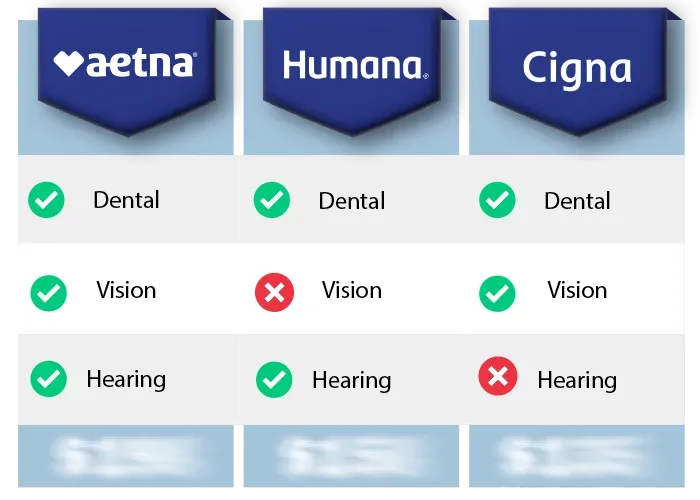

Medicare Part C, also known as Medicare Advantage, is an alternative to Original Medicare (Parts A and B) offered by private insurance companies. The premiums for Part C plans vary widely depending on the plan, the coverage it offers, and the region in which you live. These plans often include additional benefits not covered by Original Medicare, such as vision, hearing, and dental coverage.

Part D: Prescription Drug Coverage

Medicare Part D provides prescription drug coverage and is offered through private insurance companies. Like Part C, the premiums for Part D plans vary. Individuals with higher incomes may also pay an IRMAA for Part D.

Factors Influencing Medicare Insurance Premiums

Several factors can influence the amount you pay for Medicare insurance premiums, including your income, the type of Medicare plan you choose, and whether you are enrolled in a Medicare Savings Program.

Income

Your income can play a significant role in determining your Medicare insurance premiums, particularly for Parts B and D. Higher-income individuals may pay an IRMAA, increasing their monthly premium amounts.

Choice of Plan

The type of Medicare plan you choose can also impact your premiums. Original Medicare (Parts A and B) has standardized costs set by the federal government, while Medicare Advantage (Part C) and Prescription Drug Plans (Part D) premiums vary by plan and provider.

Medicare Savings Programs

Medicare Savings Programs can help eligible low-income individuals pay for their Medicare premiums and, in some cases, other out-of-pocket costs. These programs are administered by state Medicaid programs and can significantly reduce the financial burden of Medicare premiums.

Navigating Premium Changes and Enrollment Periods

Medicare insurance premiums can change annually, and it is crucial to stay informed about these changes and how they may affect your coverage and budget. Additionally, understanding the enrollment periods for Medicare is vital to ensure you are enrolled in the plans that best suit your needs and to avoid late enrollment penalties.

Annual Changes and Notices

Each year, Medicare beneficiaries receive a "Medicare & You" handbook and an Annual Notice of Change (ANOC) from their Medicare Advantage or Part D plan provider, outlining any changes to premiums, coverage, or service area for the upcoming year.

Enrollment Periods

There are specific enrollment periods for Medicare, including the Initial Enrollment Period (IEP), the Open Enrollment Period (OEP), and the Medicare Advantage Open Enrollment Period (MA-OEP). Understanding these periods and their significance is crucial for making timely and informed decisions about your Medicare coverage.

Conclusion

Navigating the landscape of Medicare insurance premiums requires a comprehensive understanding of the various parts of Medicare, the factors influencing premiums, and the enrollment periods and changes that can impact your coverage. By staying informed and actively managing your Medicare coverage, you can ensure that you have the necessary healthcare protection while also managing your healthcare budget effectively.

With careful consideration and a proactive approach, individuals can demystify the complexities of Medicare insurance premiums, making empowered decisions for their healthcare future.

Copyright © 2025 Senior Benefits Guide All Rights Reserved.

204 Church St Suite 1A, Boonton NJ 07005

Disclaimer: This website is not affiliated with the Medicare/Medicaid program or any other government entity. The information provided on this website is for informational purposes only. It is not intended to be, nor does it constitute any kind of financial advice. Please seek advice from a qualified professional prior to making any financial decisions based on the information provided. This website acts as an independent digital media & advertising publisher. This webpage is formatted as an advertorial. An advertorial is an advertisement that is written in an editorial news format. PLEASE BE AWARE THAT THIS IS AN ADVERTISEMENT AND NOT AN ACTUAL NEWS ARTICLE, BLOG, OR CONSUMER PROTECTION UPDATE. This website MAY RECEIVE PAID COMPENSATION FOR CLICKS OR SALES PRODUCED FROM THE CONTENT FOUND ON THIS WEBPAGE. This compensation may affect which companies are displayed, the placement of advertisements, and their order of appearance. Any information, discounts, or price quotations listed may not be applicable in your location or if certain requirements are not met. Additionally, our advertisers may have additional qualification requirements.

Our goal is to provide exceptional service. One of our agents may reach out to you to discuss your order, ask for feedback, and/or see if you need any assistance with your products, services, or plans, at the phone number you provided regardless of your do-not-call list status. You may opt-out of further contact at any time by simply telling our customer service team that you would no longer like to be contacted. In the event that our team is unable to reach you by phone, they may send you a text message letting you know that we called. Both our text messages and phone calls may be sent or connected utilizing automated software. Carrier charges may apply. You may opt-out of any future contact via text message by replying anytime with "STOP".

Copyright © 2025 All Rights Reserved.

Find Medicare Advantage Plans in 3 Easy Steps