🟢 Speak with an agent today!

Supplemental Medicare Plan: Navigating the Waters of Extra Coverage

Supplemental Medicare Plan: Navigating the Waters of Extra Coverage

Medicare, a cornerstone of healthcare for seniors and certain disabled individuals in the U.S., offers a foundational level of health coverage. However, like any foundational coverage, there are gaps. This is where the Supplemental Medicare Plan, often referred to as Medigap, comes into play.

Understanding the Basics of Medigap

Medigap is not just a fancy term; it's a lifeline for many. It's additional insurance purchased from private health insurance companies designed to cover the "gaps" in Original Medicare. These gaps can range from co-payments and deductibles to other out-of-pocket costs that Original Medicare doesn't cover.

To be eligible for Medigap, one must have both:

Part A (Hospital Insurance): This covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care.

Part B (Medical Insurance): This portion covers certain doctors' services, outpatient care, medical supplies, and preventive services.

Why Consider a Medigap Policy?

The primary reason individuals opt for Medigap is to offset out-of-pocket costs. While Original Medicare provides a broad range of coverage, it doesn't cover everything. Beneficiaries are often left with bills for the remaining balance. Medigap can help alleviate these costs, ensuring that beneficiaries don't have to dig deep into their pockets every time they need medical care.

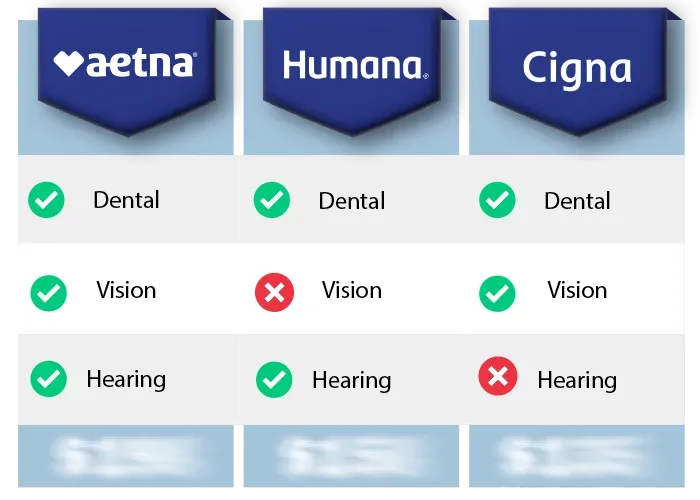

Diving Deeper: What Does Medigap Cover?

Medigap policies are standardized, meaning they offer the same basic benefits, regardless of which insurance company you purchase from. However, some Medigap policies offer additional benefits. It's essential to understand what each policy covers and compare them side by side.

For instance, while all Medigap policies cover Medicare Part A coinsurance and hospital costs (up to an additional 365 days after Medicare benefits are used), not all cover Medicare Part B excess charges or foreign travel emergencies.

Making the Right Choice: Buying a Medigap Policy

When considering a Medigap policy, timing is crucial. The best time to buy is during the Medigap Open Enrollment Period, which begins the month you're 65 or older and enrolled in Part B. During this period, an insurance company can't use medical underwriting, meaning they can't refuse to sell you any Medigap policy they offer, charge you more based on health problems, or make you wait for coverage to start.

However, if you decide to wait, there's a chance you might not be able to buy the Medigap policy you want, or you might have to pay more.

The Changing Tides: Switching or Dropping a Medigap Policy

Life is unpredictable, and your health needs can change. If you already have a Medigap policy but feel it's not the right fit, you might be considering switching. It's possible to switch, but it's essential to understand the rules and potential implications. For instance, if you're outside of the Medigap Open Enrollment Period, there's no guarantee that an insurance company will sell you a new policy if you don't meet the medical underwriting requirements.

Conclusion

The Supplemental Medicare Plan, or Medigap, offers a safety net for those looking to bridge the gap in Original Medicare coverage. Whether you're considering purchasing a policy, switching, or dropping one, it's crucial to arm yourself with knowledge. By understanding the intricacies of Medigap, you can make informed decisions that best suit your health needs and financial situation.

Copyright © 2025 Senior Benefits Guide All Rights Reserved.

204 Church St Suite 1A, Boonton NJ 07005

Disclaimer: This website is not affiliated with the Medicare/Medicaid program or any other government entity. The information provided on this website is for informational purposes only. It is not intended to be, nor does it constitute any kind of financial advice. Please seek advice from a qualified professional prior to making any financial decisions based on the information provided. This website acts as an independent digital media & advertising publisher. This webpage is formatted as an advertorial. An advertorial is an advertisement that is written in an editorial news format. PLEASE BE AWARE THAT THIS IS AN ADVERTISEMENT AND NOT AN ACTUAL NEWS ARTICLE, BLOG, OR CONSUMER PROTECTION UPDATE. This website MAY RECEIVE PAID COMPENSATION FOR CLICKS OR SALES PRODUCED FROM THE CONTENT FOUND ON THIS WEBPAGE. This compensation may affect which companies are displayed, the placement of advertisements, and their order of appearance. Any information, discounts, or price quotations listed may not be applicable in your location or if certain requirements are not met. Additionally, our advertisers may have additional qualification requirements.

Our goal is to provide exceptional service. One of our agents may reach out to you to discuss your order, ask for feedback, and/or see if you need any assistance with your products, services, or plans, at the phone number you provided regardless of your do-not-call list status. You may opt-out of further contact at any time by simply telling our customer service team that you would no longer like to be contacted. In the event that our team is unable to reach you by phone, they may send you a text message letting you know that we called. Both our text messages and phone calls may be sent or connected utilizing automated software. Carrier charges may apply. You may opt-out of any future contact via text message by replying anytime with "STOP".

Copyright © 2025 All Rights Reserved.

Find Medicare Advantage Plans in 3 Easy Steps