🟢 Speak with an agent today!

Medicare Advantage Program: Navigating the Healthscape of Tomorrow

Medicare Advantage Program: Navigating the Healthscape of Tomorrow

Introduction

The Medicare Advantage Program is a pivotal piece of the American healthcare puzzle. Introduced as an alternative to Original Medicare, this program offers beneficiaries a myriad of plan options, often inclusive of additional services not covered by traditional Medicare. As healthcare continues to evolve, understanding the nuances of the Medicare Advantage Program is paramount for seniors aiming to maximize their health benefits.

Origins and Evolution

The Medicare Advantage Program, initially known as Part C, was birthed out of the need for flexibility and customization. Original Medicare, comprised of Parts A and B, offered a standard set of benefits. However, as the healthcare landscape transformed, there arose a need for plans tailored to individual health requirements and preferences.

Plan Structure and Options

Medicare Advantage plans are offered by private insurance companies but are approved by the federal government. These plans encompass:

Health Maintenance Organizations (HMOs): These require beneficiaries to use a network of doctors and hospitals. Out-of-network care is typically not covered unless it's an emergency.

Preferred Provider Organizations (PPOs): Beneficiaries have the freedom to use any doctor or hospital, but in-network providers are less expensive.

Private Fee-for-Service (PFFS) Plans: There are no network restrictions. However, not all providers will accept these plans.

Special Needs Plans (SNPs): Tailored for those with specific diseases or characteristics.

Medical Savings Account (MSA) Plans: These combine high deductible health plans with a bank account. Medicare deposits funds into the account, which beneficiaries can use for healthcare costs.

Advantages of Medicare Advantage

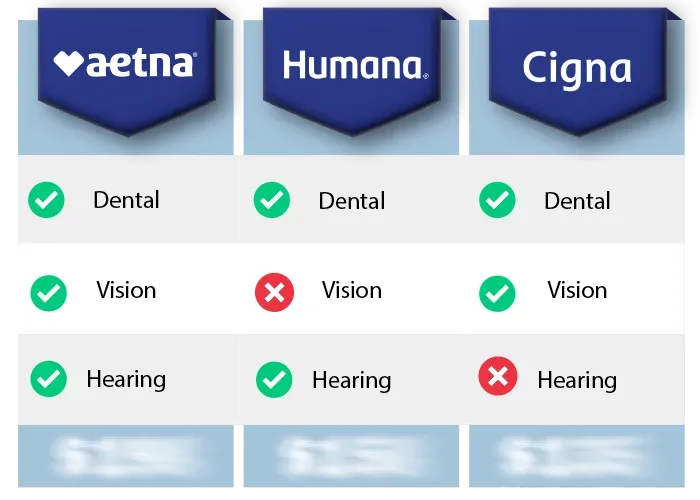

The allure of Medicare Advantage lies in its comprehensive approach. Several plans offer additional benefits, such as dental, hearing, and vision coverage. Furthermore, there's a maximum out-of-pocket limit which Original Medicare doesn't provide. This cap safeguards beneficiaries from exorbitant medical bills in case of extensive care or unforeseen medical events.

Comparing Costs

While Medicare Advantage plans often come with added perks, it's essential to understand the financial implications. Most beneficiaries will continue to pay their Part B premium, alongside any premium the Medicare Advantage plan might charge. Costs can vary based on services used, plan type, and whether the care is sought in-network or out.

Understanding Enrollment

There are specific windows when beneficiaries can enroll in or make changes to their Medicare Advantage plans:

Initial Enrollment Period (IEP): Begins three months before turning 65 and continues for three months after.

Annual Enrollment Period (AEP): Runs from October 15 to December 7 each year.

Medicare Advantage Open Enrollment Period: From January 1 to March 31, beneficiaries can switch to another Medicare Advantage plan or return to Original Medicare.

Critiques and Contemplations

While many applaud the program's flexibility, critics argue that the complexity of choices can be overwhelming for seniors. The network restrictions, especially in HMOs, can be limiting for those who require specialists or frequent particular hospitals. Therefore, it's crucial for beneficiaries to thoroughly research and perhaps consult with a healthcare advisor before selecting a plan.

Conclusion

The Medicare Advantage Program serves as a testament to the ever-evolving nature of healthcare in the U.S. While it's not a one-size-fits-all solution, for many, it offers a tailored approach that meets their unique health needs. As with all things medical, due diligence, research, and consultation are the keys to making an informed decision.

Copyright © 2025 Senior Benefits Guide All Rights Reserved.

204 Church St Suite 1A, Boonton NJ 07005

Disclaimer: This website is not affiliated with the Medicare/Medicaid program or any other government entity. The information provided on this website is for informational purposes only. It is not intended to be, nor does it constitute any kind of financial advice. Please seek advice from a qualified professional prior to making any financial decisions based on the information provided. This website acts as an independent digital media & advertising publisher. This webpage is formatted as an advertorial. An advertorial is an advertisement that is written in an editorial news format. PLEASE BE AWARE THAT THIS IS AN ADVERTISEMENT AND NOT AN ACTUAL NEWS ARTICLE, BLOG, OR CONSUMER PROTECTION UPDATE. This website MAY RECEIVE PAID COMPENSATION FOR CLICKS OR SALES PRODUCED FROM THE CONTENT FOUND ON THIS WEBPAGE. This compensation may affect which companies are displayed, the placement of advertisements, and their order of appearance. Any information, discounts, or price quotations listed may not be applicable in your location or if certain requirements are not met. Additionally, our advertisers may have additional qualification requirements.

Our goal is to provide exceptional service. One of our agents may reach out to you to discuss your order, ask for feedback, and/or see if you need any assistance with your products, services, or plans, at the phone number you provided regardless of your do-not-call list status. You may opt-out of further contact at any time by simply telling our customer service team that you would no longer like to be contacted. In the event that our team is unable to reach you by phone, they may send you a text message letting you know that we called. Both our text messages and phone calls may be sent or connected utilizing automated software. Carrier charges may apply. You may opt-out of any future contact via text message by replying anytime with "STOP".

Copyright © 2025 All Rights Reserved.

Find Medicare Advantage Plans in 3 Easy Steps